Filed Pursuant to Rule 424(b)(3)

Registration Statement No. 333-260591

BARINGS BDC, INC.

300 South Tryon Street, Suite 2500

Charlotte, NC 28202

MERGER PROPOSED—YOUR VOTE IS VERY IMPORTANT

Dear Stockholder: | | | December 28, 2021 |

You are cordially invited to attend the Special Meeting of Stockholders (the “Barings BDC Special Meeting”) of Barings BDC, Inc., a Maryland corporation (“Barings BDC”), to be held virtually on February 24, 2022, at 1:00 p.m., Eastern Time, at the following website: www.virtualshareholdermeeing.com/BBDC2022SM.

The notice of special meeting and the joint proxy statement/prospectus accompanying this letter provide an outline of the business to be conducted at the Barings BDC Special Meeting. At the Barings BDC Special Meeting, you will be asked to consider and vote upon a proposal to:

(1) | approve the issuance of shares of Barings BDC common stock, $0.001 par value per share (“Barings BDC Common Stock”), pursuant to the Agreement and Plan of Merger, dated as of September 21, 2021 (as may be amended from time to time, the “Merger Agreement”), by and among Barings BDC, Mercury Acquisition Sub, Inc., a Maryland corporation and a direct wholly-owned subsidiary of Barings BDC (“Acquisition Sub”), Sierra Income Corporation, a Maryland corporation (“Sierra”), and Barings LLC, a Delaware limited liability company and the external investment adviser to Barings BDC (“Barings”) (such proposal, the “Merger Stock Issuance Proposal”); |

(2) | approve the issuance of shares of Barings BDC Common Stock pursuant to the Merger Agreement at a price below its then-current net asset value (“NAV”) per share, if applicable (such proposal, the “Barings BDC Below NAV Issuance Proposal”); and |

(3) | approve the adjournment of the Barings BDC Special Meeting, if necessary or appropriate, to solicit additional proxies, in the event that there are insufficient votes at the time of the Barings BDC Special Meeting to approve the Merger Stock Issuance Proposal or the Barings BDC Below NAV Issuance Proposal (such proposal, the “Barings BDC Adjournment Proposal” and, together with the Merger Stock Issuance Proposal and the Barings BDC Below NAV Issuance Proposal, the “Barings BDC Proposals”). |

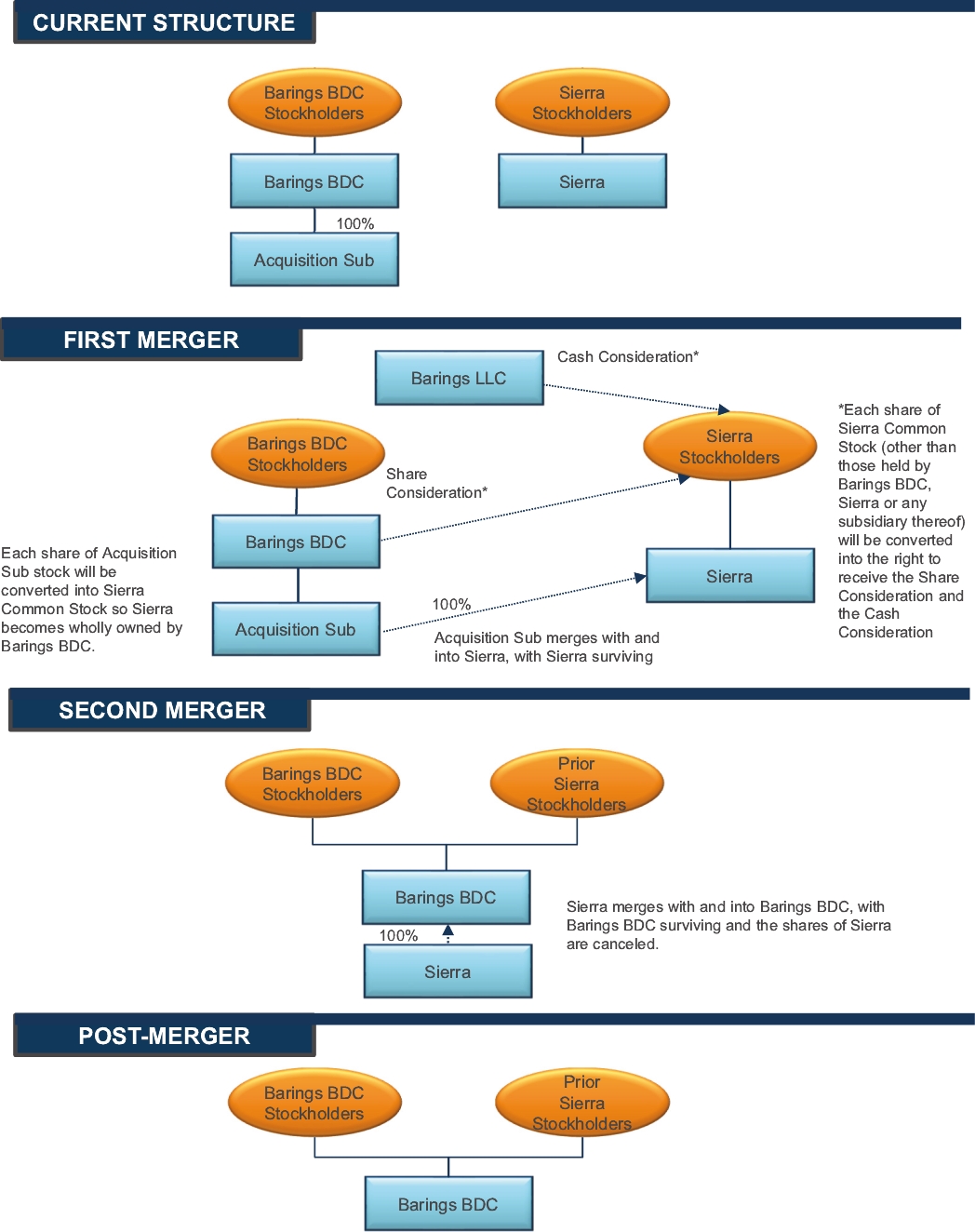

Barings BDC and Sierra are proposing a combination of both companies by a merger and related transactions pursuant to the Merger Agreement in which Acquisition Sub would merge with and into Sierra (the “First Merger”), with Sierra continuing as the surviving corporation and as a wholly-owned subsidiary of Barings BDC. Immediately after the effectiveness of the First Merger, Sierra, as the surviving corporation, will merge with and into Barings BDC (together with the First Merger, the “Merger”), with Barings BDC continuing as the surviving corporation.

Subject to the terms and conditions of the Merger Agreement, at the effective time of the First Merger, each share of Sierra common stock, $0.001 par value per share (“Sierra Common Stock”), issued and outstanding immediately prior to the effective time of the First Merger (excluding Canceled Shares (as defined below)) will be converted into the right to receive (i) $0.9783641 per share in cash, without interest, from Barings (such amount of cash, the “Cash Consideration”), and (ii) 0.44973 (the “Exchange Ratio”) of a validly issued, fully paid and non-assessable share of Barings BDC Common Stock, plus any cash in lieu of fractional shares (the “Share Consideration” and, together with the Cash Consideration, the “Merger Consideration”). For purposes of the Merger Agreement, “Canceled Shares” means all shares of Sierra Common Stock issued and outstanding immediately prior to the effective time of the First Merger that are held by a subsidiary of Sierra or held, directly or indirectly, by Barings BDC or Acquisition Sub.

The market value of the Merger Consideration will fluctuate with changes in the market price of Barings BDC Common Stock. Barings BDC urges you to obtain current market quotations of Barings BDC Common Stock. Barings BDC Common Stock trades on the New York Stock Exchange (the “NYSE”) under the ticker symbol “BBDC.” The following table shows the closing sale prices of Barings BDC Common Stock, as reported on the NYSE on September 20, 2021, the last trading day before the execution of the Merger Agreement, and on December 27, 2021, the last trading day before printing this document.

| | | Barings BDC Common Stock | |

Closing Sales Price at September 20, 2021 | | | $10.63 |

Closing Sales Price at December 27, 2021 | | | $10.91 |

Your vote is extremely important. At the Barings BDC Special Meeting, you will be asked to vote on the Merger Stock Issuance Proposal and the Barings BDC Below NAV Issuance Proposal and, if necessary or appropriate, the Barings BDC Adjournment Proposal. The approval of the Merger Stock Issuance Proposal and the Barings BDC Adjournment Proposal each requires the affirmative vote of the holders of at least a majority of votes cast by holders of shares of Barings BDC Common Stock present at the Barings BDC Special Meeting, virtually or represented by proxy, and entitled to vote thereat. The approval the Barings BDC Below NAV Issuance Proposal requires the affirmative vote of each of the following: (1) a majority of the outstanding voting securities (as used in the Investment Company Act of 1940, as amended (the “Investment Company Act”)) of Barings BDC Common Stock; and (2) a majority of the outstanding voting securities of Barings BDC Common Stock that are not held by affiliated persons of Barings BDC. For purposes of this proposal, the Investment Company Act defines a “majority of the outstanding voting securities” as the vote of the lesser of: (1) 67% or more of the voting securities of Barings BDC present at the Barings BDC Special Meeting, if the holders of more than 50% of the outstanding voting securities of Barings BDC are present virtually or represented by proxy; or (2) more than 50% of the outstanding voting securities of Barings BDC.

Abstentions and broker non-votes (if any) will (1) not be included in determining the number of votes cast and, as a result, will have no effect on the voting outcome of the Merger Stock Issuance Proposal or the Barings BDC Adjournment Proposal and (2) will have the same effect as votes “against” the Barings BDC Below NAV Issuance Proposal.

Barings, as party to the Merger Agreement, agreed to vote all shares of Barings BDC Common Stock over which it has voting power (other than in its fiduciary capacity) in favor of the Barings BDC Proposals.

After careful consideration, the Barings BDC Board unanimously approved the Merger Agreement and the transactions contemplated thereby, including the Merger, the Merger Stock Issuance Proposal and the Barings BDC Below NAV Issuance,